I believe that when most people think of the Japanese consumers, a few specific keywords leap to mind, such as “conservative” and “risk averse”. This sentiment can especially be applied to Japan’s fintech sector.

The Conservative Fintech Landscape in Japan

While fintech markets around the globe are taking off and producing unicorns in areas like digital payments, financial services, and investing, Japan still has precious few such startups of its own.

One of the few Japan-made financial tools to gain global popularity in recent years is a money saving technique invented as early as 1904 – “Kakeibo”. In an era focused on digitalization and automation, it is especially unique. Kakeibo emphasizes the need for “hand-written” accounting, as it allows for a deeper understanding of the flow of money.

Another distinctly Japanese financial habit is the Japanese people’s claim that they are the best savers in the world.

Let’s compare consumer behaviors – before US consumers make a major purchase, the first thing they consider is how to build up their credit and find a loan. In Japan, the first thought goes to saving up for that purchase.

Data from the Bank of Japan shows that half of Japanese people’s financial assets tend to be either cash or sitting in a savings account. Comparatively, in the US, the percentage of assets in savings accounts is only 12.6%, with most assets being investments in diverse areas such as stocks or funds.

The conservative Japanese attitude towards finances is indeed what has heretofore limited the domestic fintech market’s evolution compared to other countries. According to data from Crunchbase and CB Insights, the number of Japanese fintech unicorns is not in the global top ten, ranking behind India, China, Singapore, and other Asian countries.

However, Japanese financial habits along with their impact on fintech are changing.

How Japan’s Financial Habits Are Evolving

1.The Shift from Deflation to Inflation

First, it’s important to note that the key reason behind Japan’s high rate of savings can be traced to the economic bubble in the 1980’s that led to long term deflation. Since savings accounts are safer and don’t depreciate in value, it makes total sense that they would become the key financial tool for the Japanese during this time.

However, Japan’s economy has recently hit a turning point, shifting from deflation to inflation. Over the past year, Japan’s headline inflation rate has wavered between 3% and 4%, well above its long run of near 0% until 2022. In June of this year, Japan’s core inflation rate reached 3.3%, surpassing the US for the first time in eight years.

Coping with inflation is the norm for people in most countries, but it was heretofore unthinkable for Japanese.

According to a user behavior survey by Japanese fintech startup Habitto, after interviewing, nearly half of Japanese respondents aged 25 to 50 said that they had never even heard of the concept of inflation. Now, in order to cope with inflation, Japanese people need to start exploring financial management habits other than savings accounts.

2.Longevity and Financial Readiness

Another factor triggering an urgent need for financial management is that Japan has the longest average life expectancy in the world, which means that they must proactively manage their finances and prepare enough retirement funds for their old age.

3.Regulatory Openness

Japan’s recent economic liberalization has also opened up opportunities for the fintech market.

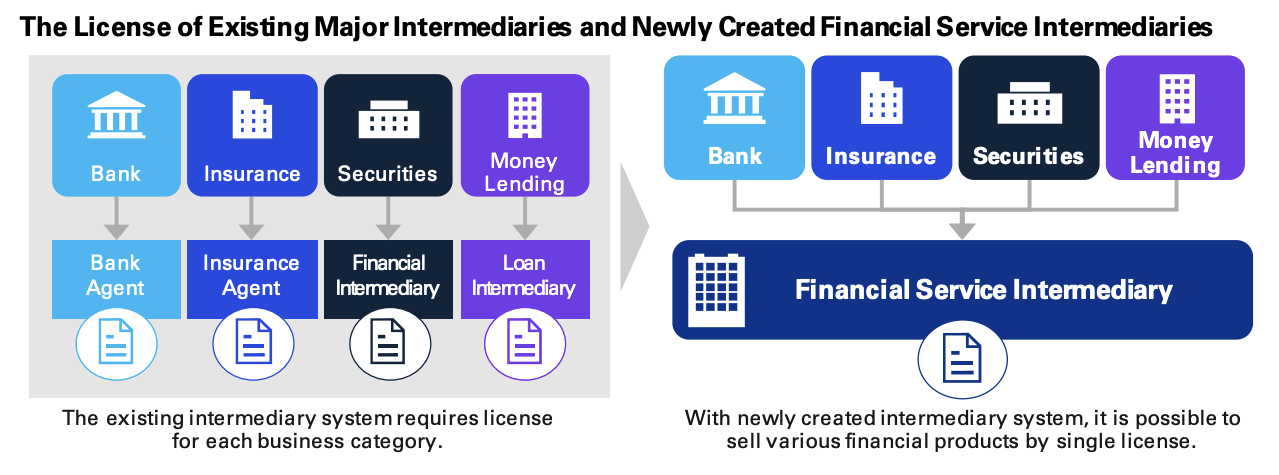

At the end of 2021, the Japanese Financial Supervisory Authority (JFSA) launched a new Intermediary License (Act on Provision of Financial Service). The license allows financial institutions to simultaneously sell banking, securities, and insurance products under a single regulatory system. In the past, banks, securities, and insurance were subject to different regulatory systems in Japan. Therefore, if you want to sell financial products, you could only obtain the corresponding licenses first, which required a long wait time and high costs to meet compliance standards.

This new intermediary bill will move Japan’s financial industry beyond clear barriers and vertical division by product towards horizontal integration. It will also greatly lower the threshold for new players to enter the market and drive innovation in financial products.

The Age of Personalized Fintech: A New Era in Japan’s Financial Landscape

In light of the overall economic environment, regulatory openness, and shifting attitudes among Japan’s youth, the financial technology market in Japan is at a pivotal juncture.

On one front, financial products are poised to diversify and expand their offerings, while Japanese consumers are venturing into the realm of financial knowledge and embracing more intricate financial tools. Faced with users who are familiar with technology but relatively “green” when it comes to financial products, there is a growing need to design financial instruments that are simpler and more user-friendly.

As a result, it is foreseeable that in the future, there will be an increasing demand for tech-enabled personal financial services in Japan. Consumers won’t need to grapple with intricate financial calculations related to the stock market, exchange rates, and other complexities. Instead, they can simply inform their financial advisor about their current assets and future financial needs. These services will then offer personalized recommendations based on the consumer’s asset situation and needs, including which financial products to purchase and the associated risks.

While the Japanese fintech market is still in the early stages with both founders and consumers still figuring out how this change will subvert decades-old habits, the biggest opportunities are often born out of the initial chaos. The first to snatch the opportunity from the chaos first is the winner.